The twelfth edition of Private Briefing, in its twelfth year of publication, brings the third part of our macroeconomic framework analysis, this time with a focus on the banking sector and the expectations for 2025 and beyond, viewed through the lens of MSMEs and farmers in need of continuous support. In addition to the macroeconomic analysis, we also examine the new Development Fund of Serbia (FZR) program designed to support family-owned businesses, and a new rural development financing initiative supported by the German KfW Development Bank. A significant program by the Provincial Secretariat for Agriculture is also featured, offering grants for the purchase of production equipment across a wide spectrum of agricultural needs.

// Agriculture in Vojvodina is one of the key drivers of regional economic development, with on-farm processing playing an increasingly important role in boosting competitiveness. In line with this, the Provincial Secretariat for Agriculture, Water Management, and Forestry of the Autonomous Province of Vojvodina has launched a call for co-financing investments aimed at adding value to primary agricultural production in 2025. The program targets active, registered agricultural holdings operating as natural persons, sole proprietors, companies, agricultural cooperatives, and complex cooperatives, as well as churches, religious communities, and monasteries.

// A total of RSD 110 million in grants is available through this call, distributed across four priority sectors: meat and dairy processing, wine and rakija production, fruit, vegetable, and medicinal herb processing, and beekeeping product processing. Individual grants range from a minimum of RSD 150,000 to a maximum of RSD 3.5 million, depending on the investment area. Grants cover up to 60% of eligible investment costs, with an increased rate of up to 70% available for specific categories, such as female farm owners, young entrepreneurs, and farms operating under challenging conditions. Eligible investments include the procurement of modern equipment and technologies needed for on-farm processing of agricultural products. Specifically, funding can be used for purchasing equipment for dairy and meat processing, including laboratory equipment, refrigeration, sterilization, and packaging devices. Investments are also eligible in equipment for wine and rakija production, as well as technologies for processing fruits, vegetables, mushrooms, oilseeds, and medicinal, aromatic, and spice plants. Special attention is also given to the beekeeping sector, where support covers equipment for honey processing and packaging, along with other bee-related products.

// Applicants can expect substantial benefits, primarily through increased productivity and improved product quality. The acquisition of new or upgraded equipment enhances operational efficiency and reduces production costs, ultimately leading to improved economic performance for farms. Furthermore, the introduction of new technologies enables producers to develop innovative and competitive products, expand market reach, and better respond to the demands of both domestic and international markets. Since up to 70% of investment costs are subsidized, the financial burden is significantly reduced, resulting in a shorter payback period and quicker realization of investment effects. In both the short and long term, this program provides meaningful support to farm income stability by increasing market resilience and enabling sustainable resource management—positively impacting both individual beneficiaries and broader rural development and living standards.

Macroeconomic Framework: Banking Sector

// The final part of the macroeconomic analysis trilogy, following the examination of global and domestic economic flows, traditionally focuses on the banking sector. In 2024, the Serbian banking sector achieved record profitability with an impressive €1.32 billion in net profit, despite a slowdown in credit activity (only +4.8% for businesses), pointing to significant structural changes in capital allocation. With inflation at 6.2% and foreign currency reserves reaching €25.3 billion, banks operated between regulatory constraints and market opportunities, leaving the economy with over RSD 2,900 trillion in unmet fixed asset financing needs and a current liquidity ratio below 0.7.

// The consolidation process continued, with the number of banks decreasing from 21 to 19 as a result of key mergers and acquisitions. The most notable transaction was AIK Banka’s acquisition of Eurobank Direktna, strengthening its position with a 13% market share and deposits exceeding €4 billion. Capital concentration continued to rise, with the top five banks controlling 63% of the sector’s total assets—a three percentage point increase compared to the previous year. Banca Intesa maintained the largest individual share at 16.1%, followed by OTP Bank and AIK with 14.3% and 12%, respectively, while UniCredit and Raiffeisen shared fourth place. Although consolidation enhances stability and enables banks to develop more sophisticated products and services, increased concentration poses challenges for smaller players facing limited access to resources and intensified competition.

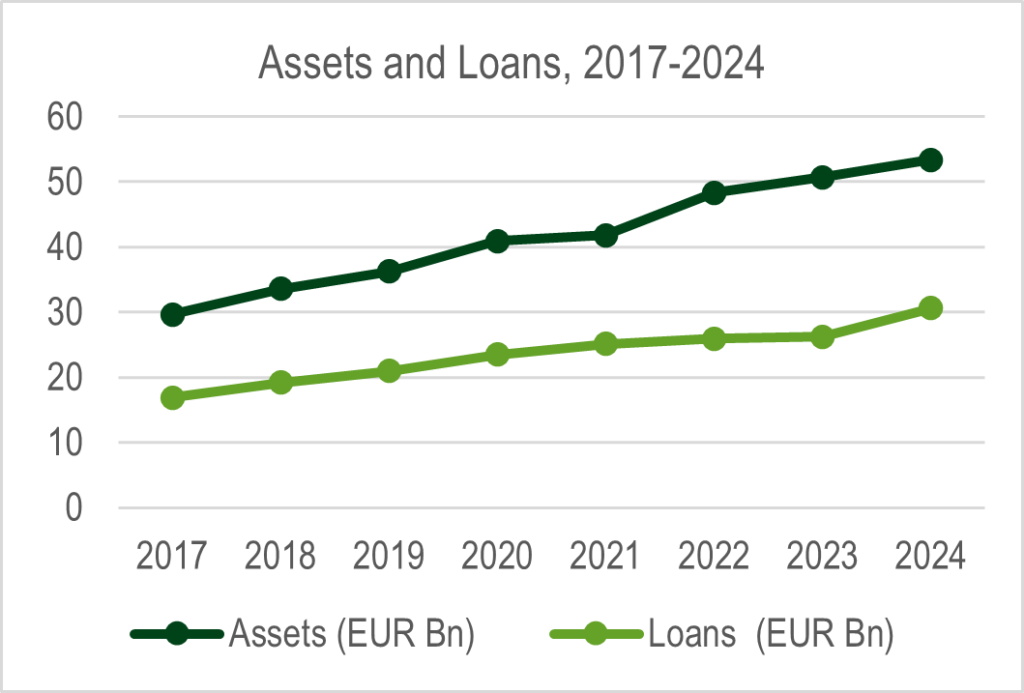

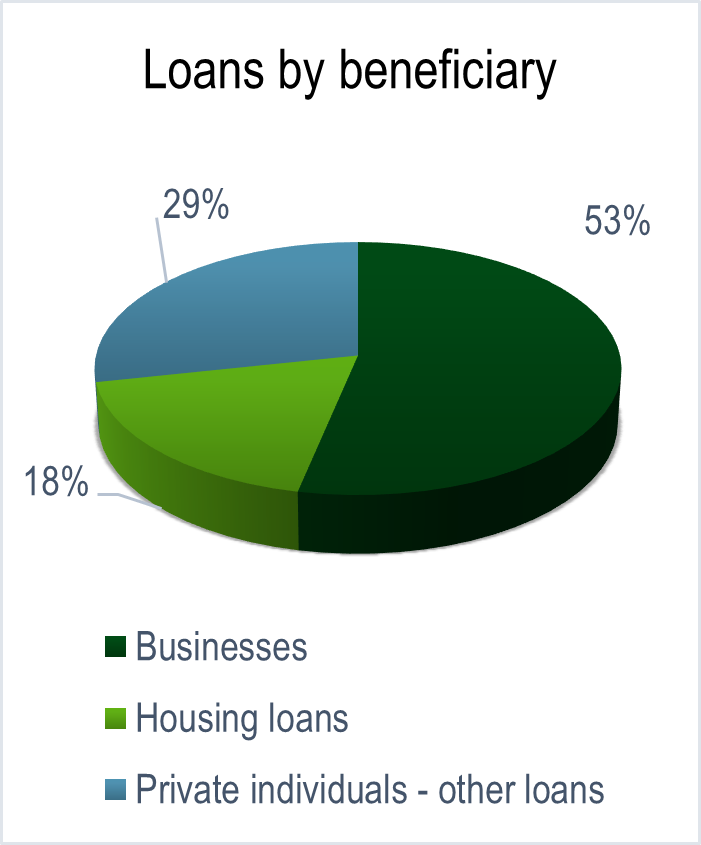

Interest margins diverged over the year: systemically important banks reduced rates for corporate clients by 0.8 percentage points, while rates for micro and small enterprises rose by 1.2 points. This discrepancy deepens the market gap and further limits access to affordable credit lines for the most vulnerable business segments. The sector’s total net balance sheet assets grew by 5.7%, reaching €53.4 billion, driven primarily by increased lending portfolios and investments in securities.

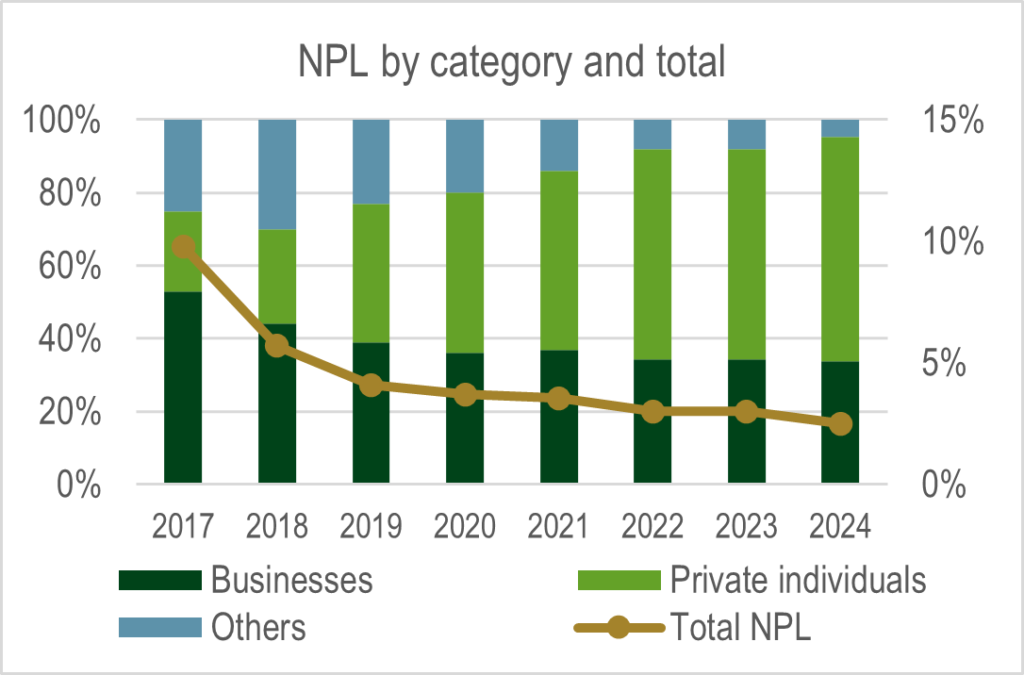

// Credit growth in 2024 was driven by corporate and household lending, while MSMEs and agriculture stagnated. Even a modest 2.6% growth in MSME lending (which holds a 59.3% share of business credit) is concerning, especially given that 83% of those funds are concentrated in liquidity support. The agricultural sector posted even weaker growth at 1.2%. In terms of portfolio quality, stability remained: the non-performing loan (NPL) ratio dropped to 2.5%, with business NPLs at 1.8% and household NPLs at 3.4%, accounting for around 60% of total NPLs. Restructured loans made up 7.2% of the business portfolio, with the highest concentrations in construction (12%) and trade (9%), reflecting lingering effects of the “permacrisis” period and financing adequacy.

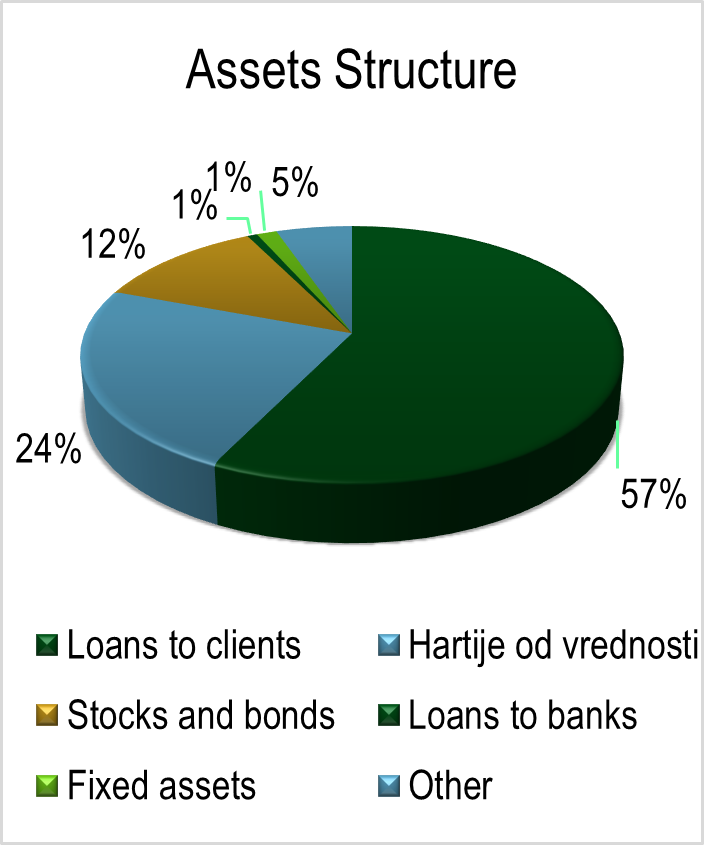

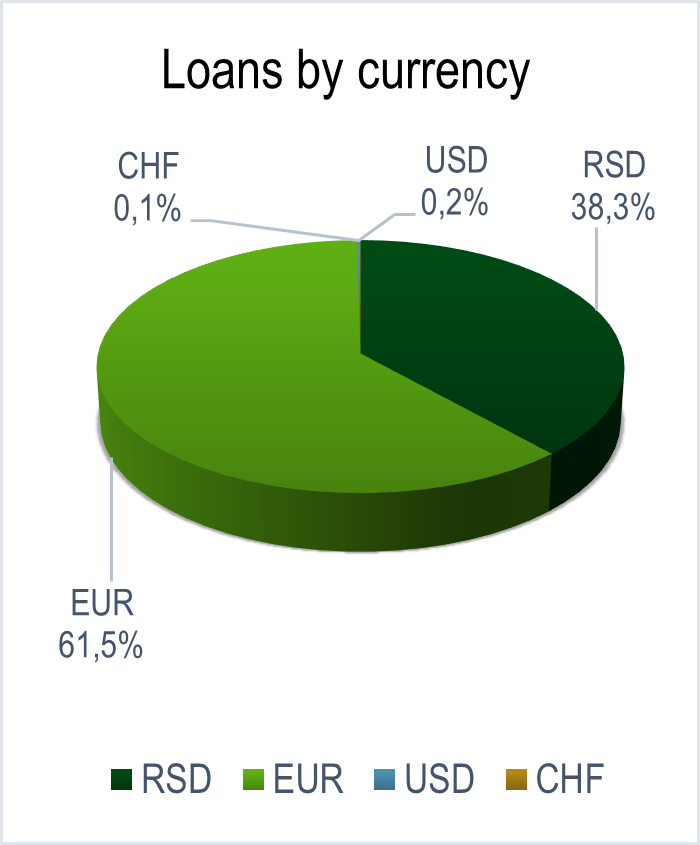

// The structure of the banking sector’s assets at the end of 2024 indicates continued dominance of client lending, increasing from 54.8% in 2023 to 57.3%. In contrast, the combined share of securities (23.4%) and cash (11.9%) declined slightly from 37.0% to 35.3%, reflecting diversification strategies. Loans to other banks, fixed assets, and other items comprised the remaining 7.4%. The currency structure remained largely foreign exchange-indexed (62%), down slightly from 63% in 2023, signaling caution toward dinar instruments despite exchange rate stabilization and NBS’s dinarization efforts. These shifts reflect a mix of NBS regulatory actions and market responses to global interest rate trends, as banks continue to balance profitability and risk in a “permacrisis” environment.

// The NBS pursued a gradual reduction in the key policy rate from 6.5% to 5.25%, reducing borrowing costs for both businesses and households. Average interest rates on dinar loans to businesses stood at 7.2%, and 6.4% for euro-indexed loans, while household loans were available at 11.8% (dinar) and 6.1% (euro-indexed). Total domestic lending rose by 8.2%, with business lending up 4.8% and household loans growing by 10.4%. This reveals a dual challenge: household consumption is largely directed toward imported goods, while domestic enterprises remain chronically underfunded for both liquidity and investments—reinforcing the need for more targeted and accelerated MSME financing.

// In 2024, Serbia’s banking sector largely remained on familiar ground. While household lending doubled the growth rate of business lending, MSMEs and agriculture continued to lack access to the modernization funds needed for competitiveness, especially in EU markets. The rapid expansion of factoring, despite annual rates exceeding 30%, highlights the liquidity demands of MSMEs and agri-businesses and signals that traditional banking models are failing to meet the needs of the real economy. Government programs, though beneficial, have been too slow in addressing regional and sectoral disparities. The rise of Open Banking and pilot initiatives for crypto-collateral offer some hope, but without systemic reforms to reduce collateral demands and increase financial inclusion, these tools remain insufficient. Ultimately, a lack of instrument diversification still limits the financial system’s capacity to support those with the greatest growth and employment potential. Beyond boosting investment readiness on the demand side—through training, advisory services, and support for preparing and executing viable development projects—a broader diversification on the supply side is essential. Whether through specialized government or international programs, long-awaited development banking, microfinance, corporate bonds, or capital markets, the message is the same: we need all of it, and we need it now. Serbia’s MSME sector must finally receive the policy priority it deserves, as the only truly sustainable engine of economic growth. Without this shift, we continue to diverge from desired development trends and miss out on the potential this vital sector clearly holds.

Development Fund: Affordable Loans for Family Businesses

// In previous editions of Private Briefing, we have frequently emphasized the importance of support provided by the Development Fund (FZR) to the domestic economy, primarily through favorable investment loans and working capital financing. Similar programs are expected this year as well. In addition to standard credit lines, FZR has introduced a new financial support program specifically aimed at family-owned businesses and family entrepreneurs. This program offers exceptionally favorable lending terms, with the goal of strengthening micro and small enterprises owned and managed by families—identified as a vital segment of a sustainable and competitive local economy.

The program targets legal entities and sole proprietors registered before December 31, 2022, operating in the fields of production and processing. A key eligibility criterion is that the company must meet requirements regarding family ownership, management, and employment. This means qualifying applicants are business entities in which family members are actively employed—whether it’s an entrepreneur working alongside a family member or a micro/small enterprise founded or staffed by family members up to the second degree of kinship, including spouses. The program is designed to improve the financial environment for family businesses, which often struggle to access affordable financing needed to expand and modernize their production capacity.

Loans may be used for a wide range of business development purposes, including the purchase of machinery, equipment, spare parts, specialized tools, as well as new computer equipment and software licenses. The program also supports investment in equipment and machinery that contributes to energy efficiency and environmental sustainability—elements increasingly relevant under modern business standards. In addition, financing is available for the purchase of business vehicles, as well as for the acquisition, adaptation, renovation, and maintenance of business, production, or storage facilities. Working capital financing is also allowed,

up to 30% of the loan amount, giving borrowers more flexibility in managing their finances. As with other DF programs, this initiative features highly favorable financial conditions. A total of RSD 500 million is available, with a maximum individual loan amount of RSD 5 million. Repayment terms extend up to 60 months, including a grace period of up to 12 months. The annual interest rate is 2.5% with a currency clause, or 1.5% for loans secured by a bank guarantee. Importantly, the loans are issued without any processing fees or commissions, further reducing the financial burden for applicants.

// Family businesses frequently face financing challenges, particularly when access to credit depends on the owner’s personal resources. This program addresses that constraint by providing access to capital under terms far more favorable than conventional commercial lending. It allows family entrepreneurs to expand operations and improve production capacity with significantly lower costs. In doing so, it enhances their ability to adapt to market pressures and remain competitive both locally and abroad. Long repayment terms and low interest rates offer a solid foundation for sustainable growth and long-term business development. The program also opens the door to modernization and digitalization, which can boost productivity, operational efficiency, and overall profitability. Its targeted approach reflects a deeper understanding of the underrepresentation of family-owned businesses in Serbia compared to developed economies—despite their proven contributions where they are more widely established. As such, this initiative is well-positioned to support a strategically important segment of the domestic economy. Glenfield consultants remain available to support applicants through project development, initial needs assessments, and securing additional financing or financial planning services.

KfW and Ministry of Economy: Structured Support to Reduce Regional Disparities

// In light of the persistent financial gap between urban and rural areas—previously addressed in multiple editions of Private Briefing—the cooperation between the German development bank KfW and Serbia’s Ministry of Economy through the “Promotion of Competitiveness in Rural Areas” program represents a critical step toward improving access to finance in rural regions. The program combines favorable loan terms, with repayment periods of up to 12 years, and technical assistance. It aims to support the diversification of local economies through investments in rural tourism, agri-food processing and marketing, green energy, digital transformation, and local infrastructure. The program’s scope extends beyond agriculture, with funding available for a wide range of development needs.

The program focuses on three priority areas: expanding access to finance for women and young entrepreneurs by reducing collateral requirements; strengthening capacities for EU market access through training and risk management advisory; and accelerating digital transformation and market linkages for local producers. Funds are disbursed through local banks that partner with KfW, using more flexible instruments than traditional credit lines. The initiative also includes elements of a hybrid model—combining loans with a grant component to support the transition to sustainable practices such as renewable energy or organic production.

A notable strength of the program lies in its robust non-financial support: mentoring networks, advisory services, and the development of local economic strategies are integrated into a broader systemic approach. In this way, the program directly and comprehensively addresses the long-standing lack of long-term and tailored financial instruments for small enterprises in rural environments. It also supports the Ministry of Economy in strengthening regional development policies, particularly through enhanced market analysis and regulatory alignment with EU standards.

// Umesto kratkoročnih i često jednokratnih subvencija, ovakav model finansiranja kombinuje pristupačne izvore sa kapacitetima za samostalan rast. Cilj nije samo povećanje obima finansiranja, već i smanjenje strukturnih razlika u pristupu razvojnim alatima. U svetlu aktuelnih nalaza o dominaciji korporativnog kreditiranja i sporom rastu plasmana ka MSP i agro sektoru, inicijative poput ove predstavljaju važan kontrapunkt. Efikasan odgovor ne mora biti isključivo tržišni ili socijalni – već, kao u ovom slučaju, i jedno i drugo. Dugoročno posmatrano, povećanje dostupnosti finansiranja uz istovremeno jačanje lokalnih kapaciteta može predstavljati osnovu za inkluzivniji i otporniji model razvoja, koji će ravnomernije raspoređivati prilike i doprineti smanjenju regionalnih nejednakosti, uz jasne i direktne koristi za krajnje korisnike, u smislu jačanja njiovog kapaciteta i konkurentnosti. Program stoga zaslužuje svaku preporuku, a budući da je u samom začetku, pratićemo razvoj instrumenata i implementaciju u narednim izdanjima.

Disclaimer: this report was prepared and published under the authority of Glenfield Training and Consulting Ltd. and is used only for informational purposes. Information that is used, have been obtained from sources that Glenfield Training and Consulting Ltd. believes to be reliable, but no guarantees their accuracy and completeness. None of the information or the proposal cannot be construed as an offer or solicitation to buy or sell. No part of this publication may be reproduced without written permission Glenfield Training and Consulting Ltd.