The March Private Briefing completes the macroeconomic trilogy with an analysis of Serbia’s banking sector, with a particular focus on the availability of capital for SMEs, the agri-sector and investment growth. In addition, three current support instruments are examined, each focused on specific sectors and areas with lower levels of access to commercial financing: the Ministry of Economy’s programme for the development of women’s entrepreneurship in rural areas, subsidised credit support in agriculture through a network of nine banks, and grants for the preservation of traditional and artistic crafts.

MoE: Women’s Entrepreneurship Development Programme in Rural Areas

// The Programme for the Support of Women’s Entrepreneurship Development in Rural Areas for 2026, implemented by the Ministry of Economy (Ministarstvo privrede), is directed at strengthening the economic position of women in rural communities through targeted support for productive activities. The programme focuses on micro enterprises whose majority founder and legal representative is a woman, on female entrepreneurs, and on cooperatives with a female majority membership, all of which conduct their activities in rural areas and operate within the productive sector. The programme is structured as an instrument aimed at contributing to the improvement of local economies, strengthening women’s entrepreneurship and creating more sustainable operating conditions in areas where access to capital and investment resources is most frequently limited. Eligible applicants are those registered with the Business Serbian Business Registers Agency (SBRA) that carry out productive activities in rural areas and use domestically sourced raw materials in their operations.

// The programme is designed to address one of the key obstacles facing women-led manufacturing enterprises in rural areas: limited access to capital for investment. In that regard, the financial support is structured to allow beneficiaries to direct funds towards those aspects of their business that carry the greatest development effect and the fastest impact on improving production. The total programme budget amounts to 50 million dinars, and grants are awarded at 100% of the acquisition value of the investment as stated in the pro forma invoice, including VAT, which makes this public call particularly attractive. The individual grant amount is set in the range of 300,000 to one million dinars. Eligible expenditure covers the procurement of new equipment, machinery and tools, new computer equipment and software licences used in the production process, as well as raw materials, whose costs may account for up to 25% of the total investment structure. This financing structure makes clear that the programme is precisely directed at investments with a direct effect on the production process, capacity growth and quality improvement, thereby incentivising the transition from a constrained or less efficient operating model to a more stable and technologically advanced form of production.

// For female entrepreneurs seeking to consolidate their operations, increase production volumes, or improve the quality and continuity of delivery, this programme represents a highly functional development mechanism, in that it enables investments which small manufacturing enterprises and female entrepreneurs frequently defer precisely because of a lack of own funds and the constraints they encounter when attempting to secure financing through traditional sources. At a support intensity of 100%, the programme is highly effective for those who do reach it. On the other hand, its coverage is limited. The budget covers approximately 100 beneficiaries, representing a penetration rate of below 0,2%. It may therefore be worth considering whether, instead of 100% subsidy, scaling through partial co-financing of the investment, partial interest subsidy on commercial loans, or risk-sharing arrangements would allow the instrument to reach a substantially wider pool of beneficiaries — within the same budgetary framework and without undermining the developmental logic of a programme that, through investment in appropriate equipment and the modernisation of the production process, can deliver immediate gains in productivity, work organisation, quality consistency, and overall market competitiveness and business sustainability.

Macroeconomic Overview: The Banking Sector

// The final part of the macroeconomic trilogy, which in the January edition mapped global fragmentation lines and strategic repositioning, and in the February edition examined the slowdown in domestic growth to 2,3% and the consolidation themes that will define 2026, traditionally concludes with an analysis of the banking sector. The banking sector is not merely a mirror of economic trends; it is also the transmission mechanism between macroeconomic conditions and the capacity of the real economy. It is precisely that transmission function — examined through the parameters and indicators that define the sector’s operational framework — that forms the core of this analysis. As some data have been updated as of the end of the third quarter, projections through year-end have been used for certain indicators. This, with all due reservations regarding data reliability, does not materially affect the conclusions and insights of the analysis.

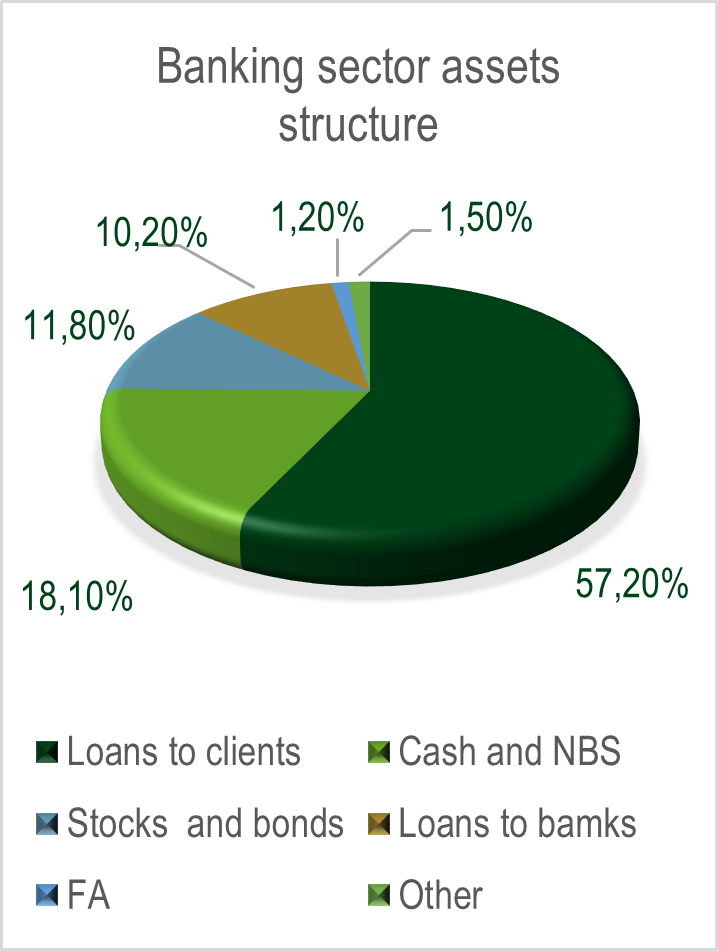

Serbia’s banking sector closed 2025 with total net balance sheet assets that reached 58,6 billion euros by the end of the third quarter, compared with 53,4 billion at the end of 2024, representing growth of almost 10% over a period of just nine months. The sector’s structure remained unchanged in terms of the number of participants relative to the previous year, with the count of 19 institutions stabilising following years of consolidation. Concentration remains high, with the six largest banks controlling nearly three quarters of total sector assets; Banca Intesa at 15,4% and OTP banka at 14,7% remain firmly at the top, while Raiffeisen banka at 11,3%, UniCredit at 10,7%, and AIK and NLB at 10,4% and 10,3% respectively complete the group of systemically significant participants

// Sector profitability in 2025 continued along the trajectory set by the record year of 2024, now established on a new and higher plateau. Based on data for the first nine months of 2025, the sector’s net profit amounts to 133,6 billion dinars, or approximately 1,14 billion euros. On an annualised basis, this corresponds to an estimate of around 1,53 billion euros, which would represent a new record and growth of more than 15% relative to the 1,32 billion euros recorded in 2024. The annualised return on assets (ROA) stands at 2,60%, and the return on equity (ROE) at 19,21%, with the ROE of the six largest banks reaching an even higher 21,3%. These indicators remain several times above the European average, where ROA stands at around 0,75% and ROE at around 10,5%. Total negative profit positions in the sector amount to less than one million euros, which is statistically negligible. The sector’s net interest margin on an annualised basis stands at 3,60%, with interest income remaining the dominant item, accounting for 72% of total net operating income, while 28% is derived from fees and commissions

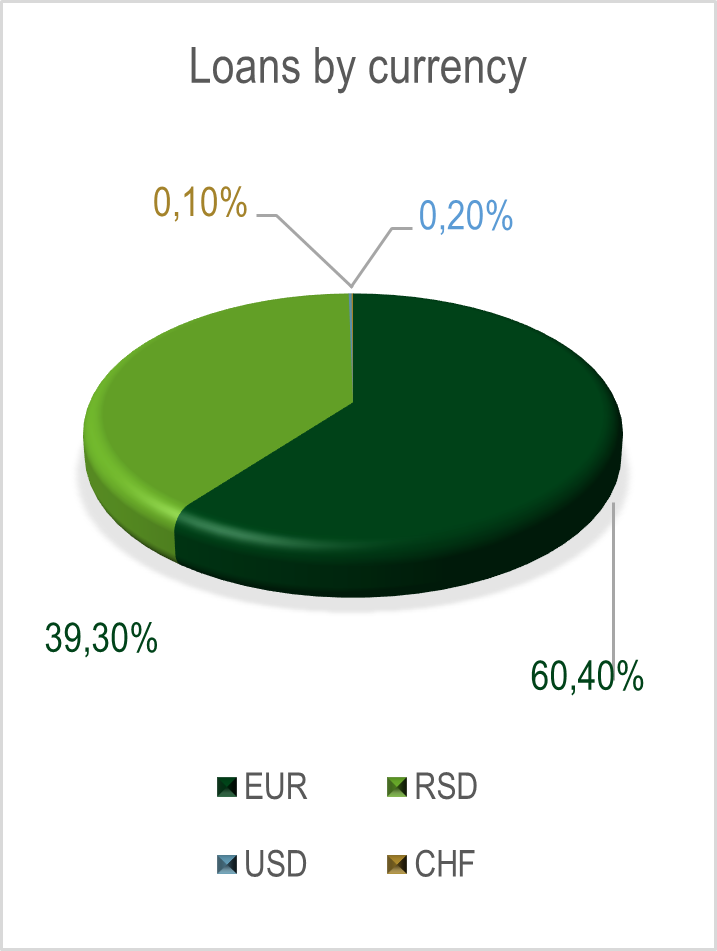

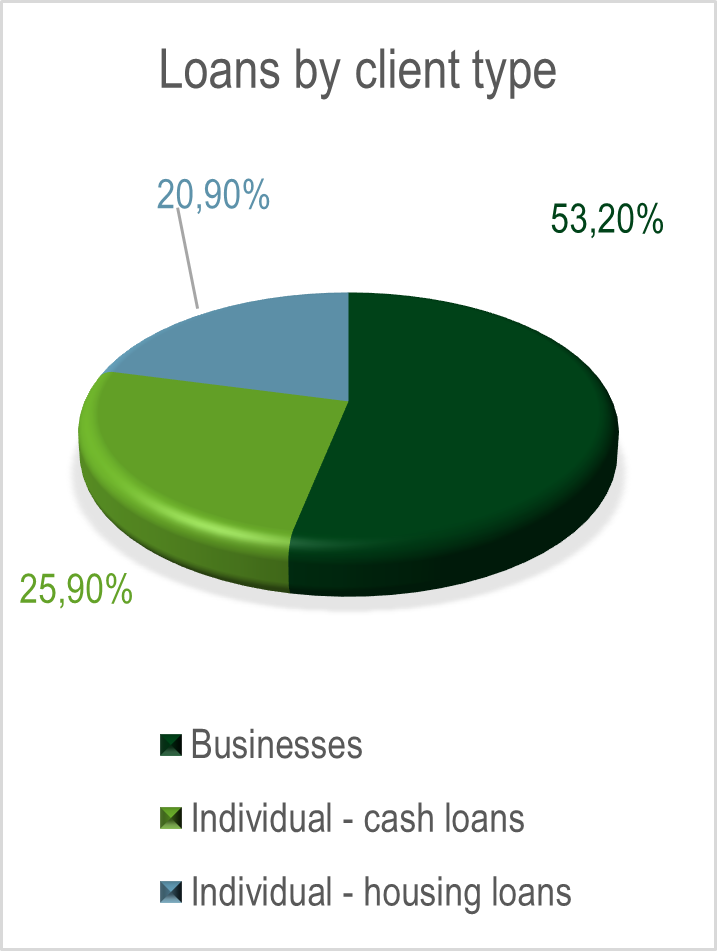

Total loans to the private sector recorded year-on-year growth of 15,4% at the end of December 2025, compared with 8,2% in 2024. Household lending grew by as much as 19,5%, while placements to the corporate sector rose by 11,3%. SMEs represent, by total volume, the dominant segment of corporate lending, accounting for 60,6% of total placements to the economy, with year-on-year growth of 11,2%. However, given that SMEs account for 99,4% of the total number of enterprises in Serbia, this means that almost 40% of all bank lending to the economy is directed at 0,6% of the total enterprise count. Dinarisation of placements reached a record 39,3% of the total portfolio, an increase of 6,3 percentage points compared with the end of 2024. Average interest rates on dinar-denominated loans to businesses remained in the range of 6 to 8%, and on euro-indexed loans from 4 to 5%, while housing loans continued to grow under demand pressure and with limited regulatory intervention from the National Bank of Serbia (NBS).

The share of non-performing loans fell to a historic low of 2,11% in the third quarter of 2025, compared with 2,5% at the end of 2024 and 3,0% at the end of 2023. The NPL ratio for corporate lending stands at 1,4%, and for household lending at 2,7%. This trend is determined by multiple factors: tightened approval standards, continued restructuring, and the growth of the overall portfolio, which statistically “dilutes” the share of non-performing placements. The total value of deposits (both those of individuals and coprorate) has grown approximately 10% y.o.y. and reached 42,8 billion euros, reflecting both confidence in the banking system and the limited availability of alternative savings and investment instruments. The sector’s digital transformation continues through investment by all systemically significant banks in platform services and open banking; however, the only natively digital bank continues to operate at a loss, confirming that the fintech model has yet to find its profitable formula within the domestic banking context.

// The monetary policy of the National Bank of Serbia (NBS) throughout 2025 was characterised by stability and caution. The key policy rate remained unchanged at 5,75%, at which level it has stood since September 2024, on the assessment that inflationary risks remain present. The NBS nonetheless acted actively through a series of regulatory instruments that directly affected the cost and availability of credit. The Law on the Protection of Financial Service Users introduced systemic caps on interest rates for individual borrowers, as a result of which rates on credit cards were reduced from 22,3% to 14,7%, and on current account overdrafts from 27,9% to 17,1%. From September 2025, a dedicated loan model for lower-income citizens was introduced, which in Q4 produced the strongest quarter-on-quarter increase in household lending since 2008.

Taking stock of the year as a whole, 2025 confirms what previous analyses suggested: Serbia’s banking sector is highly profitable, well-capitalised, liquid and stable — which is unambiguously good news. However, the indicators also point to a structural gap between the profit potential of the banks and their effect on the real economy, since high profitability and an exceptionally healthy sector do not automatically translate into a high degree of financing availability for businesses, and even less so once the criteria of tenor and type of financing are factored in. Credit expansion, in terms of its structure, is far from closing the gap between the needs of SMEs and the agri-sector for long-term and investment financing on one hand, and the portfolio profile that banks prefer on the other. The sector is increasingly successful at generating income within a very narrow band of the highest-quality market segments, while the penetration and availability of financing as fuel for economic development remains very low. The fact that 0,6% of enterprises by number absorb almost 40% of all corporate lending is not in itself an anomaly — large enterprises carry larger projects and larger volumes — but it is to a considerable degree driven by persistent structural inhibitors to lending in the SME segment. Among these, perceived risk and collateral requirements are arguably the most significant, but a lack of diversification and specialisation in support provision is also a contributing factor. Both research and practice confirm that segments such as women-led businesses, youth-owned enterprises, rural businesses and social enterprises are clearly defined and structurally underfinanced segments whose risk profile is considerably better than dominant assessment models suggest. In that context, although the main business support programmes realised through the Development Fund (FZR), KfW, EBRD, EIB and other credit lines and EU grants — which are examined regularly in the editions of Private Briefing — remain a significant mechanism seeking to compensate for what market logic alone does not provide, a systemic response to the identified imbalance, in the form of a tectonic reorientation of financing flows towards the real economy, is still awaited. Support programmes, particularly those that combine a financial component with non-financial services, are also proving important for strengthening demand-side capacities — that is, the ability of enterprises to prepare, present, finance and implement sustainable projects. The Social Impact Finance initiatives that we monitor and participate in have already built part of the infrastructure for the financial implementation of the next generation of credit instruments, grounded in incentives and very concrete, measurable social impact indicators spanning a range of inclusion dimensions for young people, women and other groups with traditionally limited participation in the labour market. On the other side of the equation, the “green” aspects of lending — introduced long ago — have moved from the domain of creating “savings-based benefits” for borrowers into the domain of obligation, with a growing body of regulation that now effectively levies penalties on emissions and prices in energy inefficiency. In this way, both the “E” and the “S” of ESG have become part of the market reality of both the real and the financial sector.

// Within the broader landscape of trends that are emerging — or have already arrived — increasingly deep digitalisation and data management systems represent a resource of immense value. Banks that have used the development initiatives and programmes of international development institutions to build, with technical assistance, the infrastructure and methodology for managing the vast volumes of data collected through their operations are now positioned to scale financing models from their own potential. Drawing on data-driven decision-making, segmentation and targeted outreach, this places them in a position to unlock the enormous potential of the market and thereby achieve a win-win-win outcome across the triangle of their own business performance, their clients and the national economy through meaningful growth rates. It is precisely for this reason that the support programmes, development credit lines and new financing models examined in Private Briefing remain important — not as a substitute for the banking sector, but as a corrective wherever market logic alone does not produce sufficient developmental effect, and as a bridge between the capacities of the banking sector and those of SMEs.

DAP: 900 Million Dinars in Subsidised Interest Through a Network of Nine Banks

// The Directorate for Agrarian Payments (UAP — Uprava za agrarna plaćanja) issued a public call for credit support in agriculture for 2026 in early March, with a total budget of 900 million dinars. This is a programme that differs in mechanism from conventional grants, in that the state does not pay a direct non-repayable contribution to the beneficiary, but rather subsidises the interest on a loan that the beneficiary takes with a commercial bank. In this way, the overall effect on beneficiaries is significantly scaled, as the support budget is used to bring the cost of servicing the loan well below the market rate, with the bank subsequently submitting a claim for the interest subsidy to the Ministry. An important operational detail is that nine commercial banks with agreements with the Ministry participate in the programme, which makes access geographically and institutionally broad enough to generate an effect across the entire territory of the country. At the same time, this offers applicants the opportunity to factor in additional service criteria when selecting the commercial bank through which they will submit their application and realise the financing.

Eligibility for credit support extends to holders of commercial family agricultural holdings, entrepreneurs and agricultural cooperatives with at least five members, provided they are registered in the Register of Agricultural Holdings with active status and a renewed registration for 2026. The eligible purposes are set broadly across sectors and include livestock development through the purchase of animals, arable farming, fruit growing, viticulture, vegetable growing and floriculture, investment in mechanisation and equipment, the purchase of animal feed, and the acquisition of quality breeding heifers and cows up to five years of age. The maximum loan amount is 6 million dinars for natural persons and entrepreneurs, and 18 million dinars for legal entities, with a repayment period of up to three years, or up to five years for certain purposes, and with the option of a grace period.

The interest rate for the beneficiary is fixed and directly reflects the logic of policy: the standard rate is 3% per annum, while privileged categories receive considerably more favourable terms. Young farmers up to the age of 40, women and holders of agricultural holdings in areas with difficult working conditions pay 1%, as do those purchasing breeding heifers and cows, while the interest rate for the purchase of fertilisers is zero. Rates at this level represent a meaningful concession, given that on a three-year loan at the maximum amount of 6 million dinars, the difference between the market and the subsidised interest rate can easily exceed the value available through many equipment grants. The programme, furthermore, does not require a cash deposit as a form of security, making it more accessible to holdings with limited liquid reserves.

One important operational detail is that applications are processed in the order in which documentation is received, with eligibility determined until the available funds are exhausted. In the context of a budget of 900 million dinars that may be closed before 30 June if funds run out before that date, and taking into account that the average subsidy rate is around 3 to 4% and that the average loan, given the approximate split of 70% natural persons and entrepreneurs and 30% legal entities, can be estimated at around 8 million dinars, the total capacity of the programme amounts between 800 and 1.000 beneficiaries. Divided across nine banks, that is 90 to 100 applications per bank over the entire duration of the call, or less than one complete application set per branch considerng the full network of close to 900 outlets.

// Viewed in the context of the broader set of support instruments available to farmers, this programme fits naturally as a complement to IPARD support and to the grants of the Provincial Secretariat or national agri-incentives. For a holding planning an investment in mechanisation that does not meet the thresholds for IPARD Measure 1, or does not wish to undertake the demanding preparation of an IPARD project, subsidised-interest credit support may be the right tool for the current year. At the same time, for those who are in the process of preparing an IPARD project, this line can cover purchases that are not eligible under IPARD or that are needed before the IPARD grant arrives. Combining the two instruments requires careful consideration of timing, purposes and amounts, but when carried out correctly, the result is a substantially more efficient use of available resources than either programme alone can provide, and given the breadth of the implementation network, an early response is strongly recommended.

Ministry of Economy: Support for the Preservation of Traditional and Artistic Crafts

// The public call for the award of grants implemented by the Ministry of Economy of the Republic of Serbia (Ministarstvo privrede) under the Programme for the Support of the Development of Traditional and Artistic Crafts and Home-Based Work Activities in 2026 is an instrument directed at the preservation of traditional craft skills and the encouragement of entrepreneurship development in this segment. The programme simultaneously aims to improve competitiveness and preserve cultural heritage through support for the modernisation of production and the preservation of authentic working techniques, and is intended for micro and small enterprises, entrepreneurs and cooperatives active in this field.

The programme is directed at economic entities operating in the field of traditional and artistic crafts and home-based work activities, with a clear focus on those whose activities generate added value based on traditional knowledge and production techniques. Entities eligible to participate include registered micro and small enterprises, entrepreneurs and cooperatives, subject to the mandatory condition of holding a valid certificate for the conduct of these activities, issued by the Ministry of Economy. Additionally, beneficiaries must meet criteria relating to active status, the timely settlement of public obligations and compliance with state aid rules, which ensures that funds are directed towards entities with the basic capacity for effective investment implementation and long-term sustainable operations.

The subject of the public call is the financing of the procurement of new production equipment and raw materials directly in service of conducting traditional and artistic craft activities and home-based work activities. Eligible equipment must be intended for professional use within the production process, while raw materials are understood to include primary materials and semi-finished goods that are further processed into finished products. At the same time, the programme establishes clear restrictions on ineligible costs, including transport, import, financial services, maintenance, training and transactions between related parties.

The programme’s financial framework is directed at smaller investments of limited scope, calibrated to the needs of micro and small business entities. The total budget amounts to 25 million dinars, with individual project grants ranging from 80.000 to 300.000 dinars, at a support intensity of 100% of eligible costs including VAT. This financing structure entirely eliminates the need for own contribution within the defined limit, while at the same time leaving open the possibility for beneficiaries planning larger investments to secure additional funds to cover the difference, something that in practice requires careful planning of the scope and priorities of investment.

// The total reach of the programme can be estimated at just over 120 beneficiaries, assuming an average grant amount of 200.000 dinars. That figure represents approximately 10% of the total number of qualified applicants registered as traditional crafts or home-based work activities, which gives the programme a considerably different weight in terms of coverage. This public call represents a particularly favourable opportunity for programme participants to strengthen their business through direct enhancement of production capacities, with minimal or no own financial contribution. Through the financing of equipment and raw material procurement, the programme provides a concrete incentive for craft workshops to improve efficiency, increase production volumes and stabilise operations. At the same time, through its support for activities that carry cultural and local significance, participants not only improve their own competitiveness but actively contribute to the preservation of traditional crafts — something of particular relevance at a time when digitalisation and AI are absorbing a significant share of industrial and administrative work.

Disclaimer: this report was prepared and published under the authority of Glenfield Training and Consulting Ltd. and is used only for informational purposes. Information that is used, have been obtained from sources that Glenfield Training and Consulting Ltd. believes to be reliable, but no guarantees their accuracy and completeness. None of the information or the proposal cannot be construed as an offer or solicitation to buy or sell. No part of this publication may be reproduced without written permission Glenfield Training and Consulting Ltd.