The third Private Briefing in 2024 brings the final chapter of the trilogy of analyses on the macroeconomic framework, in the form of the analysis of the banking sector and expectations for this year and the immediate future. After a two-year hiatus, we present an analysis of the new IPARD call, which has improved effects both in terms of the amount and the purposes of support. Support for businesses comes in the form of an analysis of DFs’ permanent working capital loans, supported by the EIB, and to show that rural does not mean only agriculture, we bring an analysis of support programs for rural tourism.

// In an environment where access to medium-term or long-term loans for micro, small, and medium-sized enterprises (MSMEs) remains limited, support in financing permanent working capital can be crucial for the sustainability of a business. This is precisely the goal of the Development Fund (DF) program, which, through a new form of financing in partnership with the EIB, recently enables loans for permanent working capital under particularly favourable conditions.

// The loans are intended for a wide range of purposes, from the purchase of raw materials, supplies, and inventory to financing current liabilities – production costs and obligations to suppliers, to receivables from customers. The anticipated amounts of funds for end users in this new call go up to as much as 1.45 billion dinars, or 12 million EUR. The interest rates are the same for all users, regardless of their legal form, and the indicative interest rate is 3.586% annually, which is more than favourable, especially for smaller businesses and smaller amounts of financing. The maturity of the loans is up to 5 years, within which there is a grace period of up to 12 months, and it will be the same for all users regardless of their legal form, with monthly repayment. Businesses with fewer than 250 employees as well as mid-caps, defined as companies with a minimum of 250 employees and less than 3000 employees, who have registered their predominant activity as one of the activities listed by the European Investment Bank and who have achieved positive financial results in the last two years, are eligible to use funds under this credit line of the European Investment Bank.

// Permanent working capital represents a resource necessary for the effective enhancement of user business activities. It enables the maintenance of business continuity and an increase in competitive capability through stability, planned operations, and significant expansion of capacity and production volume with an increase in the quantity of raw materials, and opening of new locations. At the same time, continuous capacity for the procurement of raw materials or goods improves the company’s position with suppliers and leads to a reduction in costs, thereby affecting profitability and capital accumulation for further growth and development. An additional aspect is the increase in the company’s capacity for risk management, namely unexpected costs, fluctuations in raw material prices, or market changes. The purpose of loans for permanent working capital, with very well-measured repayment terms of 5 years and favourable interest rates, makes this financing option a favourable solution for financing the current liabilities of end-users, which can have a significant effect on the long-term improvement of capacity and competitiveness. A prerequisite for achieving these goals is certainly a good investment plan along with careful analysis of the economic framework and market potential. The mentioned parameters are provided within the business plan, which is an integral part of the documentation for applying to the Fund, and for quality preparation of the business plan and the entire application, cooperation with consultants with many years of experience in preparing projects for Fund support can be beneficial.

Macroeconomic Overview: The Banking Sector

// Following the macroeconomic analysis of trends and projections of key market movements and expectations for 2023, with a focus on global trends and general economic movements in Serbia in the previous two editions, this one turns to the analysis of trends and projections for the banking sector, as the last element of the trilogy that frames the overall business environment. Given that annual results are partially available, as some are published with a delay, some analyses are based on data up to the end of the third quarter of 2023, but the trends are clearly depicted even with this limitation. The expectations for 2023 were in the direction of continued consolidation and recovery of the economic environment. However, a series of negative events collectively referred to as “permacrisis,” led by inflation and disrupted distribution channels from the Far East, and supported by the regional crisis in Ukraine, have taken on global dimensions in the post-COVID environment, and the global financial system has radically reacted to impulses from the environment. Given the high level of integration of the domestic financial system, trends have spilled over and left consequences locally, of course in conjunction with local specificities.

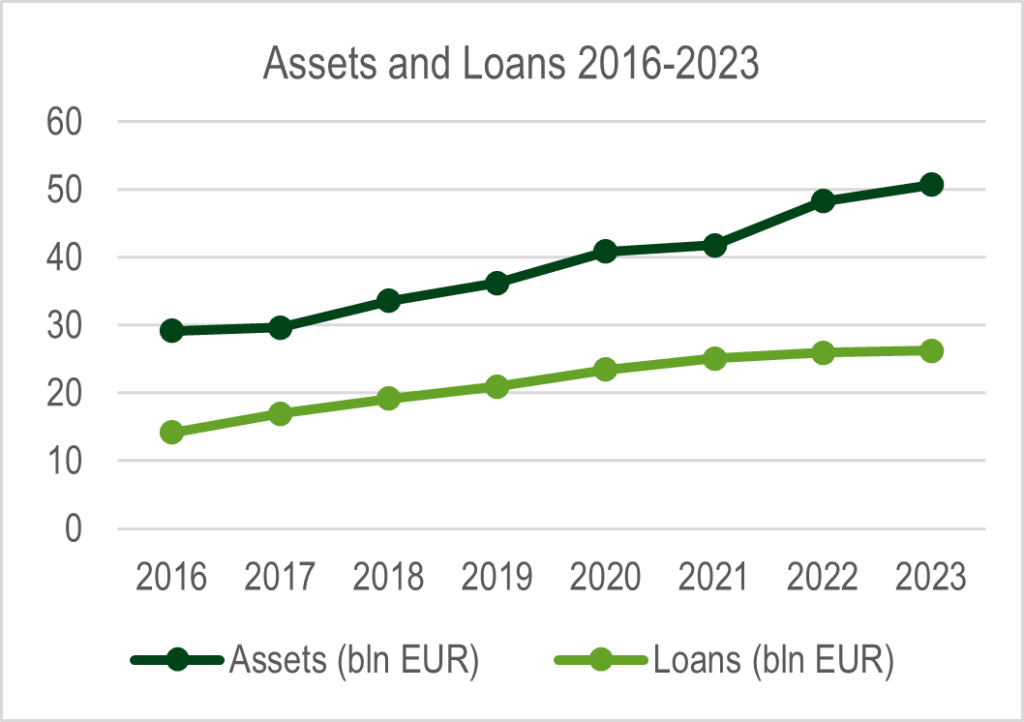

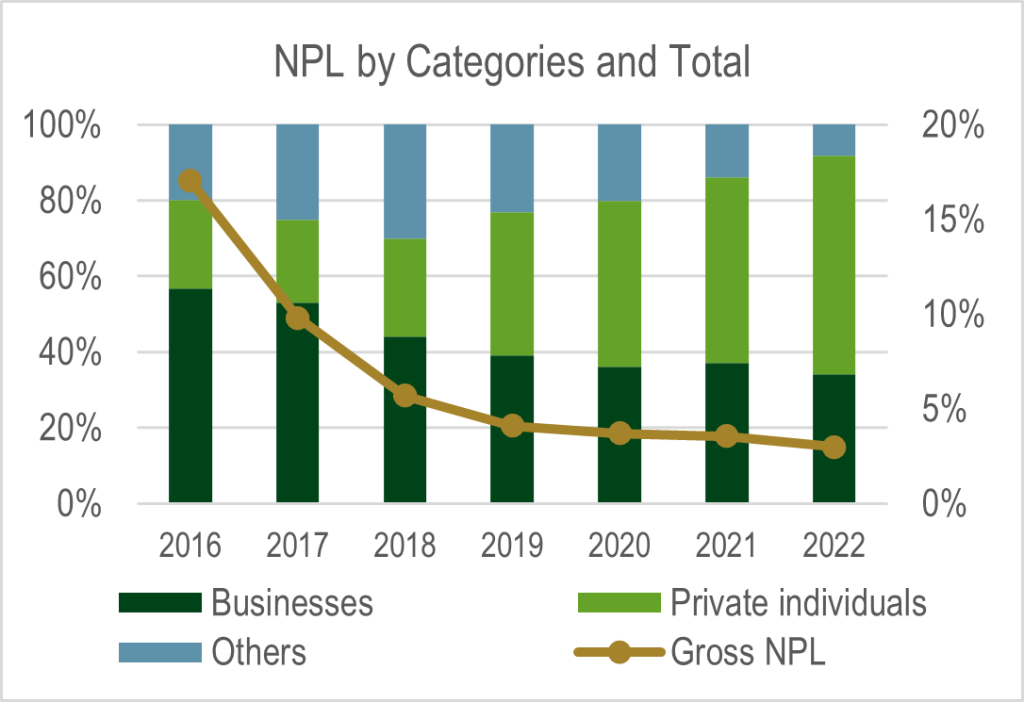

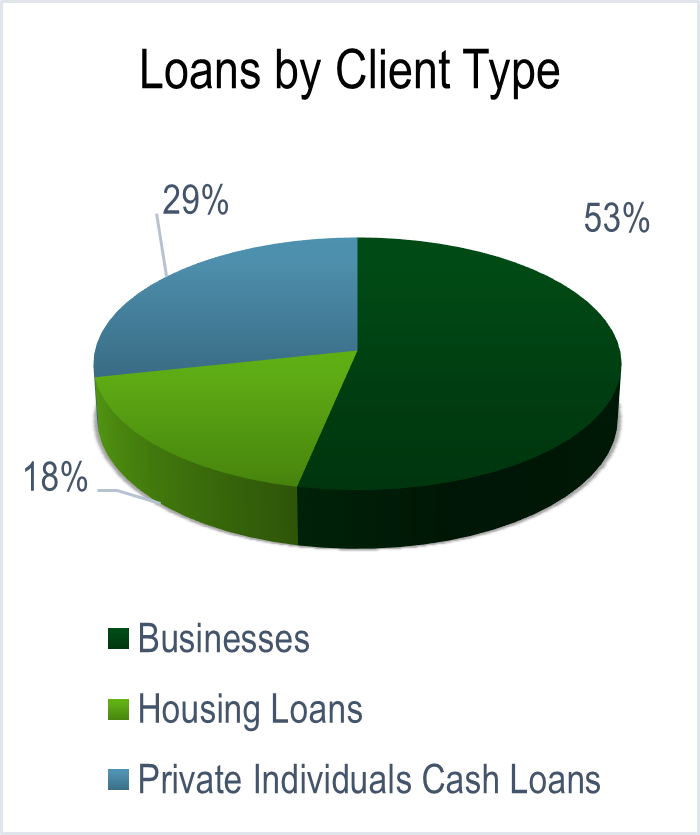

// In line with the processes and trends of previous years, the banking sector continued consolidation, with numerous processes of agreed and approved mergers during 2023 being finalized, for now. The total number of registered banks has thus reached 20, compared to 22 at the end of the previous year, with a slightly reduced number of employees just under 22,000, 1.7% less than the previous year, and about 50.6 billion euros in net balance sheet assets, which is an increase of about 2 billion euros or about 4% compared to the end of 2022. The combined market share of the top three banks has exceeded about 41%, the top four banks hold about 50% of total assets, and the top five over 60%, so the sector’s concentration remains significant. Individually, Banca Intesa has the largest share with about 15.6%, followed by OTP with 13.5%, and Raiffeisen and UniCredit share third and fourth place with about 11% share, while NLB Komercijalna takes fifth place with close to 10%. The share of non-performing loans (NPLs) at the end of 2023 has ceased to decline and remained practically unchanged from the year before, at 3%. A larger share of NPLs still comes from the retail sector. The stability of the portfolio quality can be attributed to the tightened credit policies of banks, as well as measures by the NBS which, anticipating a deterioration in repayment quality, allowed banks at the end of 2022 to restructure claims from debtors facing repayment difficulties, i.e., to extend repayment periods for cash, consumer, and housing loans.

// Unlike the trend of decreasing the reference interest rate during 2021 and stabilization in 2022, due to the global effects of rising inflation, which in Serbia at the beginning of 2023 was 15.1% and by the end of the year 8%, the reference interest rate gradually increased from 5.25% in January to 6.5% in December, reflecting the efforts of the National Bank of Serbia to respond to inflationary pressures. This led to an increase in borrowing costs and interest rates on loans, as well as a slowdown in lending activity, so that the average interest rate on dinar loans to the economy at the end of the year reached 8.4%, and on loans to the population 12.7%, while rates on euro-indexed loans were on average 7.1% for the economy and 6.4% for the population. In this structure of borrowing costs, the impact of housing loans, whose price was reduced by 1.5 percentage points, partly due to the NBS’s decision to limit interest rates, and partly to stop the trend of a decrease in the share of this category of loans in newly approved loans, which fell from almost one-fifth to 15% as a result of the intense rise in real estate prices.

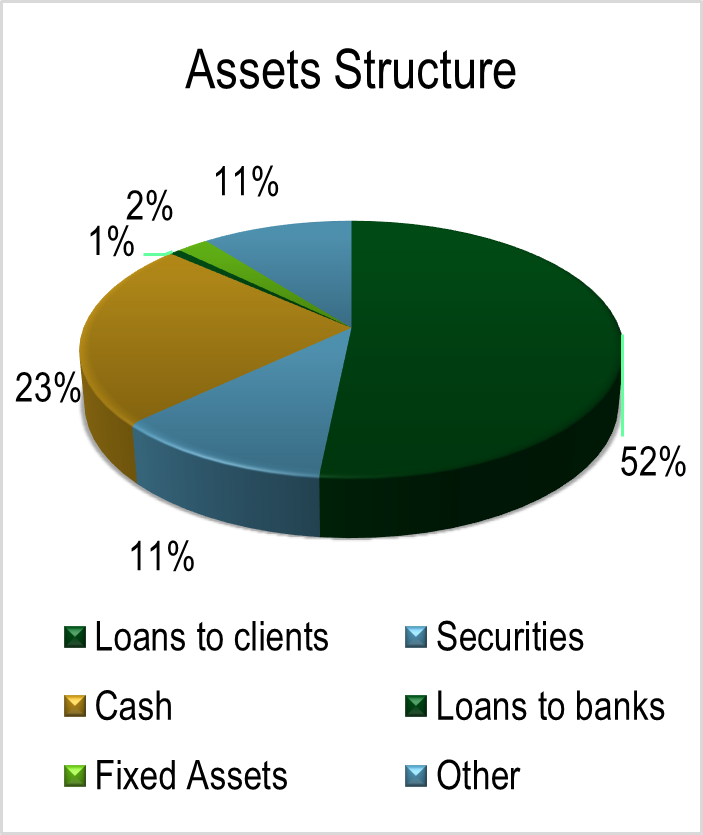

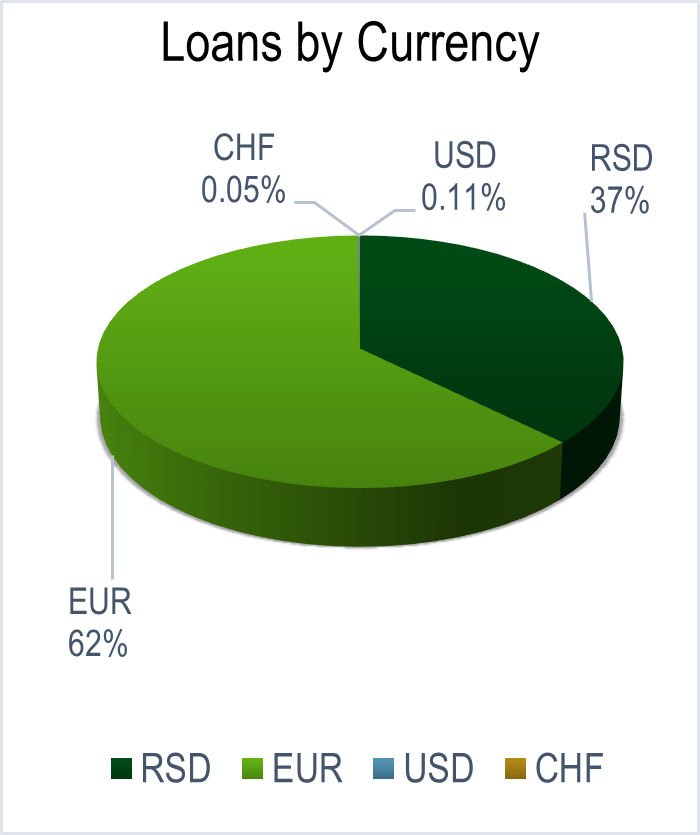

Total domestic loans, excluding the effect of the exchange rate change, increased in 2023 by 1.1%, with loans to the economy increasing by 0.9%, and loans to the population by 1.2%. This actual slowdown during 2023 is certainly a result of higher interest rates due to the tightening of monetary policies, but also stricter bank policies. In corporate loans, significant impacts also came from the maturities of loans under guarantee schemes. Regarding the overall structure of the banking sector’s assets, there was a slight decline in the dominance of the Client Loans category, which decreased from over 56% in the previous year to 52% in 2023. On the other hand, the categories of Securities and Cash together recorded an increase in share from about 31% to 34%. The currency structure of bank portfolios remains predominantly foreign currency-indexed, at a stable 62%, slightly below 63% from the previous year.

// Regarding general impacts on development and operations, the trend of digitization within the banking sector continues within the global “AI” paradigm analysed in the January Private Briefing. Additionally, “personalization” is a word that was mentioned throughout 2023 and became one of the expected main inputs for further sector development. In the context of banking services and products, this should bring a model of significant adjustments according to customer needs. In the case of the domestic economy, needs change relatively slowly, primarily relating to easier access to long-term funds to compensate for the constant lack of financing sources for fixed assets. Furthermore, the needs of domestic MSMEs and entrepreneurs are very clearly expressed towards strengthening positions for taking positions with foreign partners, in the constant trend of “nearsourcing” which has almost completely settled as the way the global economy responded to crises and their impacts on logistical routes. This also requires significant investments and long-term, or at least medium-term, funds for building, strengthening, and maintaining new positions. To respond to these needs, further strengthening of internal capacities will be necessary, especially considering the mentioned personalization of offers for clients. Sector consolidation and increasing concentration inevitably affect competitiveness and potentially reduce the inclusiveness of support. Thus, it is to be expected that challenges in terms of potential relaxation of access to quality financing for the economy will continue in the near future. This makes various alternative financing methods, constantly relevant. Factoring, especially in combination with digital platforms, experienced a real boom in 2022 and crystallized in 2023 as a model with high risk appetite, offsetting the risk by the high interest rates which include risk premiums. Despite the extremely high cost, is simply overwhelmed with demand primarily due to significantly more relaxed conditions and criteria for financing approval, which just shows the real preferences of users. There are also alternative investment funds, especially for fast-growing businesses. Of course, special economic support programs that effectively absorb a large part of the financing segment for small businesses and entrepreneurs hold their standard place in the offer, which we regularly analyze right here.

IPARD 3: Additional Support Models in the Largest Farmers’ Support Package

// After a two-year hiatus, it is time to analyse the new public call within the framework of the IPARD III programme, under the auspices of Measure 1 – Investments in the physical assets of agricultural holdings. This call also marks the start of a new phase of IPARD support, which, with a budget of 288 million euros from EU funds and an additional 90 million from the Serbian budget, could potentially generate a new 580 million euros of investments in the agro sector, assuming an average grant of 65%.

In addition to the four measures accredited under IPARD II, the new cycle introduces additional opportunities, including Measure 4 – Agroecology and climate-responsible agriculture, Measure 5 – Implementation of local rural development strategies through the LEADER approach, as well as Measure 6 – Investments in rural public infrastructure. This year’s IPARD III call also expands the sectors supported through the programme, including fisheries, processing of cereals and industrial crops, with a special focus on rural tourism, direct sales of agricultural and local products, and services in rural areas. By introducing new sectors and those supported through Measure 7, the IPARD III

programme continues with diversification, and a significant novelty is the condition that specific requirements for the production sector are observed at the end of the investment, instead of at the beginning, which should facilitate a greater number of users in achieving support. Also, a broadly set list of eligible investments and costs, and the introduction of the possibility of supporting new technologies such as agricultural drones or special vehicles, signals that the programme remains open to a wider range of projects, giving users significant freedom in planning and implementing improvements they recognise as important for the realisation of development plans.

With a total budget of 4.8 billion dinars, which can cover up to two-thirds of the value of investments, the current call within Measure 1 can generate significant incentives for improvements and the transition of agricultural producers into a new category of competitiveness and efficiency. Eligibility extends to individuals – holders of commercial family agricultural households, entrepreneurs, companies, and agricultural cooperatives, and the applicant must have proof of professional knowledge or experience in agriculture. The call brings a significantly expanded support model through the possibility of financing for various types of investments that include the construction and equipment of facilities in primary agricultural production, as well as the establishment of production and rootstock orchards of fruits and grapes. The amount of incentives varies from 60% to 75% of eligible investment costs, depending on several factors, including the status of young farmers, organic production, the location of the farm, and investment type.

//

The scope and extent of support once again confirm that IPARD calls enable significant improvements that lead to increased productivity and efficiency, growth in competitiveness, reduction in operating costs, and increased capacity to compete in the global market, through subsidising the acquisition of physical assets of holdings that certainly require significant investments. Given the established standards, but also the scope of potential support, the application process remains demanding, as it requires a detailed business plan and accompanying documentation already at the project application stage. This represents the first step towards achieving the right to support, after which follows the implementation of the investment and the request for payment approval. As IPARD is now in its third iteration, a significant set of experiences has been gathered from previous calls, among them the most common mistakes in preparing applications. These certainly include submitting incomplete project documentation, as well as the lack of detailed analysis and mere estimation. This implies both a careful analysis of the requirements and an understanding of the specific conditions related to the sector being invested in, and an assessment of the capacity to implement the planned activities. Specifically, for advice and support in preparing your project, from the preparation of project documentation to the implementation of the investment, our team of experts is at your disposal, so you can seize the opportunity to materialise the support IPARD provides. Additionally, we are available for initial needs analysis processes, as well as for securing necessary pre-financing.

Ministry of Tourism: Significant Support for Rural Tourism

// On the wave of pandemic restrictions in previous years, domestic tourism offerings, along with the support provided for them, have gained additional importance. Initially, the key goal was to support those who faced a drop in turnover, but in the last two years, it’s evident that the focus has shifted towards generating capacity to meet increased demand, by enriching and enhancing the quality and breadth of the offerings. In line with such trends, the Ministry of Tourism and Youth has announced a Public Call for the allocation of incentives aimed at the development and enhancement of rural tourism and hospitality with the goal of encouraging activities that contribute to the improvement of tourist offerings and infrastructure in rural areas of Serbia. Eligible applicants are commercial entities, other legal entities, or entrepreneurs engaged in hospitality activities in accommodation facilities in rural areas, namely farms, ethnic houses, and rural tourist households, as well as individuals conducting hospitality activities in rural tourist households, provided that the facilities are registered in the e-Tourist system.

The incentives can be used for a wide range of offer improvements, which include the construction of new and extension of existing hospitality and related facilities, reconstruction, renovation, adaptation, or investment maintenance of hospitality facilities, landscaping of yards, purchase of garden furniture, as well as equipping

hospitality facilities to enhance the hospitality offer and expand accommodation capacities. Users are obliged to co-finance the project with at least 10% of the total project value, while the maximum amount of incentives per project can reach 2,9 million dinars. Projects should be implemented within 12 months from the date of the incentive funds payment.

// This Public Call opens exceptional opportunities for the enhancement of rural tourism and hospitality, offering financial support for projects that will contribute to the development and diversification of the tourist offer in rural areas. With the available financial resources, users can significantly improve the quality and accessibility of their services, investing only 10% of their own funds for markedly noticeable effects. Additionally, the support can also have a wider positive impact on increasing tourist traffic, sustainable development, and creating new employment opportunities for the local population. Since the incentives are designed to minimally burden the user while delivering significant results and motivating investments in a sector that is of growing importance for the economic development of rural areas, while simultaneously promoting sustainable development and the conservation of cultural and natural heritage, the call deserves every recommendation.

Disclaimer: this report was prepared and published under the authority of Glenfield Training and Consulting Ltd. and is used only for informational purposes. Information that is used, have been obtained from sources that Glenfield Training and Consulting Ltd. believes to be reliable, but no guarantees their accuracy and completeness. None of the information or the proposal cannot be construed as an offer or solicitation to buy or sell. No part of this publication may be reproduced without written permission Glenfield Training and Consulting Ltd.