June 2026 Private Briefing analyses instruments at both ends of the financing spectrum, from grants for larger processing investments to favourable loans for women’s entrepreneurship and land acquisition. The focus is on the Serbian Development Agency’s support programme for the automation of capacities in the food industry, the DFV credit line for women-led businesses and the provincial call for the purchase of agricultural land. And then, in the midst of a summer heatwave, we launch a seasonal special dedicated to hydration. It is, of course, well known that conditions like these call for plenty of fluids, so we are opening an entire trilogy devoted precisely toliquidity, and how to manage it.

// The Development Fund of Vojvodina has announced a call for long-term loans to support women’s entrepreneurship, subsidised by the Provincial Secretariat for Economy and Tourism. Eligible applicants include micro, small and medium-sized companies in which a woman holds at least 51% ownership and is also the responsible person, as well as women entrepreneurs operating as sole proprietors, provided that they are based in AP Vojvodina and that the investment is implemented on its territory. Already at the level of beneficiary definition, it is clear that this is a targeted instrument designed to direct development capital towards a segment of the economy that often shows solid business potential, but operates with a narrower scope for financing growth due to limited access to finance in general.

// The purpose of the loans is broad enough to support that objective and respond to the actual needs of small businesses in a growth phase, as the funds are approved for financing investment projects, in amounts ranging from 300.000 to 10 million dinars, in line with the applicant’s creditworthiness. The programme gains additional practical value from the fact that the loans are approved without mandatory own participation, with maturities of up to seven years and a grace period of up to 24 months. The interest structure further increases the usability of the programme, as for loans with a currency clause the interest rate stands at 2% plus six-month EURIBOR, reduced by 1% when the loan is secured by a commercial bank guarantee, while for dinar loans the interest rate is variable and linked to the repo rate, with a margin of 0,50% for the III and IV development groups, and 0,80% for the I and II development groups. The Provincial Secretariat will additionally subsidise regular interest in 2026, which further lowers the cost of capital for beneficiaries for whom access to more affordable financing is often the key condition for launching an investment at all. In addition, the absence of a loan processing fee further reduces the total cost associated with the investment, making it more cost-effective, its return faster and its beneficiaries more competitive.

// The programme is not conceived as a broad support mechanism, but as a relatively precisely calibrated development instrument that requires a basic level of business stability and the capacity to carry the investment through, which is reflected in the requirement to submit a business plan under the Fund’s model. At the same time, the favourable cost of funding and the grace period leave beneficiaries with more room for the investment to be implemented first, put into operation and begin generating results. In an environment in which adequate access to finance is often the main obstacle to modernisation, capacity expansion or equipment procurement, this lending framework represents more than a source of funds, because it creates scope for a development step to be taken earlier and with less pressure on current liquidity. That is why this call deserves the attention of women entrepreneurs planning modernisation, business expansion or a new investment, because it combines an amount that can be development-relevant, conditions that are not overly rigid, and an institutional framework that still insists on the project’s business sustainability.

SDA: Grants for Investments in the Food Sector

// The Serbian Development Agency has published a call for incentive funding to attract direct investment in the automation of existing capacities in the food industry, within a dedicated line for the technological upgrading of one of the most important sectors of the domestic processing industry. The programme covers investments in the tangible and intangible assets of food industry companies, with the aims of improving productivity, increasing the number of domestic cooperants and expanding the use of domestically sourced raw materials, making it an instrument that ties the investment to a broader development effect, both within the company and across its supply chain.

The call prescribes that funds may be awarded for investment projects with a minimum value of 1 million euros, with the beneficiary required to cover at least 25% of eligible costs from its own resources or from other sources not containing state aid. These eligibility criteria, alongside the other eliminatory conditions, indicate that the programme targets companies with an established level of operational and financial order and the capacity to carry an investment through a medium-term development cycle. Eligible purposes include plants, machinery and equipment, as well as patents, standardisation and licences,

while passenger vehicles and transport vehicles are explicitly excluded. Eligible costs are those incurred from the date of application until the project implementation deadline, and all assets acquired must be new. The maximum grant is 20% of eligible costs, though additional financing through other state aid programmes is permitted, provided the combined total does not exceed 50% for large, 60% for medium-sized and 70% for small companies.

The programme’s seriousness is further reflected in the content of the application and business plan, which goes well beyond a list of equipment to be purchased. The applicant must explain the full economic and market architecture of the investment, covering the project description and implementation approach, objectives and resulting products, reasons for automation, a SWOT analysis, ownership and organisational structure, key clients, competitive advantages and market position. Further requirements include data on competitors, suppliers and market trends, sales and export plans, procurement plans, a breakdown of the planned increase in the use of domestic raw materials and the number of domestic cooperants.

// The technical section requires an overview of the existing and planned product range and production volumes, the effects of the new technology on capacity, productivity and the degree of processing, a description of the technological process, equipment selection, the implementation site and environmental and occupational safety measures. The financial section requires projections of revenues, costs, financing sources, net present value, internal rate of return, payback period, and projected balance sheets, income statements and cash flows.

// It is precisely in this breadth of requirements that the intended beneficiary profile becomes clear. The assessment criteria cover the investor’s references, investment amount and type, the technological level of the activity, prior supplier cooperation and the planned share of domestic suppliers, the effects on capacity and degree of processing, the financial and market assessment, existing production levels and planned productivity gains, and data on raw material sourcing and cooperants. The programme essentially targets companies that understand automation as a strategic development step rather than an isolated technical purchase. The project implementation deadline is three years, extendable to five upon a reasoned request, leaving realistic scope for more complex interventions and phased implementation. For food sector companies seeking a measurable technological shift, deeper reliance on domestic raw materials and stronger links with the local cooperative chain, this call warrants serious consideration.

Market and competitive analysis, business strategy preparation, financial projections, net present value and internal rate of return are precisely the areas in which the Glenfield team has long-standing experience and thousands of completed projects. Therefore, for an initial eligibility assessment and support in structuring the application, Glenfield consultants are available.

The Summer Hydration Trilogy E1: Early Symptoms

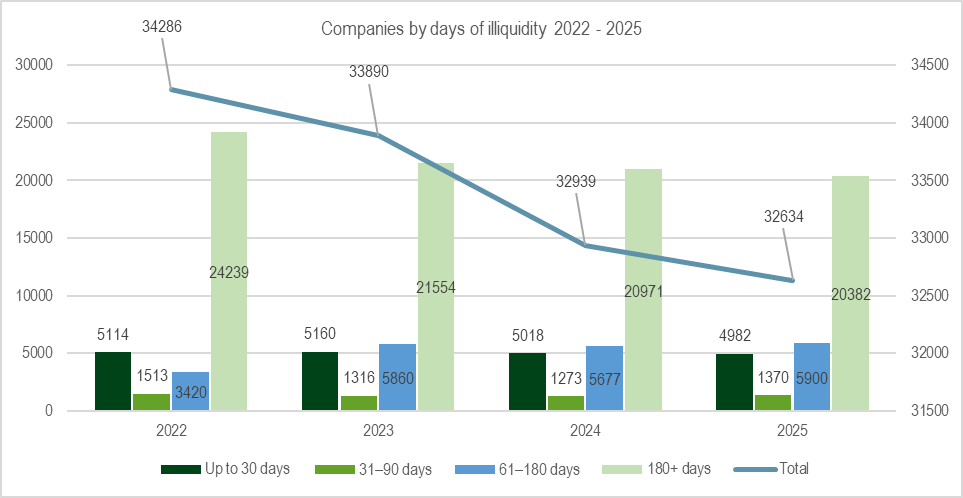

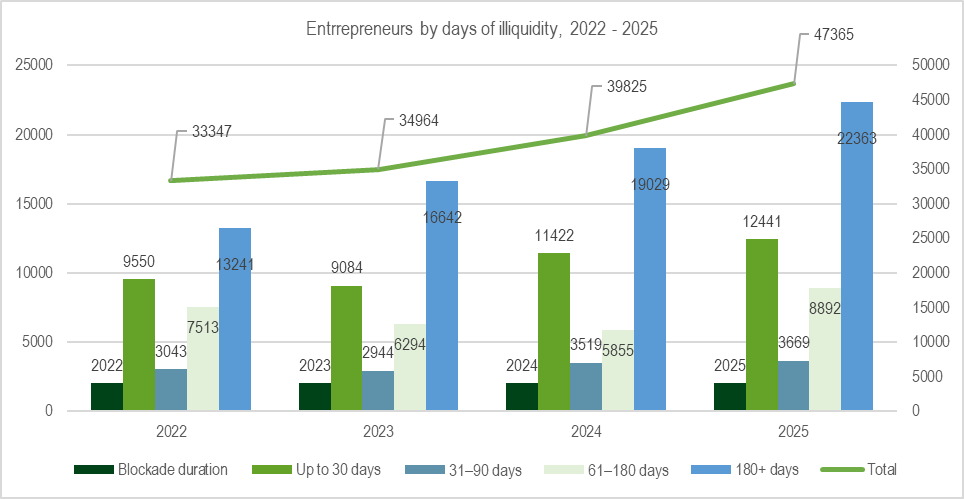

// Illiquidity is a particularly specific business phenomenon. It very often goes unnoticed and unaddressed until the acute symptom arrives, the “heatstroke” of an account blockade. When that phenomenon becomes widespread, it can also be read as a chronic condition affecting an entire population, or in our case, an entire economy. And that is the inspiration for this series, the APR report on blocked accounts, as the most precise and reliable data source, with a sample coverage of 100% of the market. Blocked accounts speak to the individual weaknesses of companies and entrepreneurs, and the report in question can very much indicate the quality of cash flow management, the degree of financial preparedness and the availability of instruments that could ease such pressures before they escalate into serious operational disruption, at the level of the market as a whole. According to APR data, at the end of October 2025, there were 136.857 registered companies and 368.446 entrepreneurs in Serbia, while at the same time 20.382 companies and 22.363 entrepreneurs were subject to blockades lasting longer than 180 days, giving a share of 15% of companies and 6% of entrepreneurs. These figures represent a serious signal of financial vulnerability across a substantial segment of the economy, and of the pressing need for hydration solutions.

It is also important to note that the problem does not remain confined to the zone of the longest blockades. In 2025, 5.900 companies were recorded in blockade for 61 to 180 days, 1.370 in the 31 to 60 day interval and 4.982 in blockades of up to 30 days. Among entrepreneurs, the picture is more difficult, with 8.892 entities in the 61 to 180 day interval, 3.669 in the 31 to 60 day zone and as many as 12.441 in blockades of up to 30 days. When shorter blockades are included, the picture widens further, with a total of 32.634 companies, or 23,8% of the total, and 47.365 entrepreneurs, or 12,9%, subject to some form of blockade. This means in practice that illiquidity is not a condition reserved for a small number of entities already deep in difficulty, but one that spans the full spectrum of business, from early signs of financial instability to prolonged blockade as a chronic to terminal symptom. In that sense, an account blockade is more the final stage of a process than an isolated event, typically preceded by extended weak collections, a mismatch between inflows and obligations and the postponement of financial decisions that should have been taken earlier

Looking beyond absolute figures to trends reveals additional complexity. Among entrepreneurs, the number of entities in blockade exceeding 180 days grew from 13.241 in 2022 to 16.642 in 2023, 19.029 in 2024 and 22.363 in 2025. Among companies, the number declined from 24.239 in 2022 to 21.554 in 2023 and has since stagnated at a similar level. At first glance, this may suggest that companies were gradually moving out of the deepest zone of illiquidity, while entrepreneurs were increasingly entering it. However, APR began compulsory deregistration of companies for inactivity precisely in 2022, which is not the case for entrepreneurs.

In practical terms, between four and five thousand companies are removed from the register each year, which means that the trends on the charts share, unfortunately, a great deal in common, with growth among entrepreneurs visible across almost all illiquidity intervals. This distribution suggests that a significant part of the entrepreneurial sector operates under constant liquidity pressure, with the problem appearing not only when the business is already seriously at risk, but much earlier, through short and medium-term blockades that point to the fragility of day-to-day financial functioning.

// In that context, illiquidity is clearly a signal of deeper problems rather than just a financial indicator. The high numbers of blocked entities point to an environment in which internal cash flow management mechanisms are not yet sufficiently developed and available external support instruments are not always accessible, used in a timely manner or well enough aligned with the real needs of the economy. We therefore read the data beyond the count of entities already in blockade, and consider how wide the gap is between early warning signals and the point at which the problem escalates into enforcement proceedings. And that is our starting point for the great Summer Hydration Trilogy. In this first episode we went deep into the analysis and established a diagnosis. Most analyses do not get this far, but we are just getting started, and the next two episodes will be devoted to solutions for that diagnosis. In the next episode we explain the DIY approach, how to help yourself through sound financial management, liquidity planning and strengthening management’s capacity to recognise and address the problem adequately. Stay tuned for E2.

DFV: Supporting Farm Development Through Land Acquisition

// The Development Fund of Vojvodina has announced a call for long-term loans for the purchase of agricultural land, with the primary objective of creating conditions for intensifying agricultural production and raising the efficiency and competitiveness of individual agricultural holdings. Eligible applicants are natural persons who are the holders of an active commercial family agricultural holding on the territory of AP Vojvodina, aged under 70. The investment itself must also be implemented within the Province, and the purpose is clearly defined as the purchase of agricultural land for the consolidation of registered holdings. Therein lies the development logic of this credit line, as the purchase of additional parcels finances not only an asset, but the long-term improvement of the holding’s productive base.

Loan amounts range from 300.000 to 20 million dinars, in line with the applicant’s creditworthiness, making this line usable both for modest purchases and for more substantial consolidation of land holdings. For loans with a currency clause, the interest rate stands at 2% plus six-month EURIBOR, reduced by 1% for loans secured by a commercial bank guarantee,

while for dinar loans the rate is variable and linked to the NBS reference rate with a margin of 0,80%. The repayment period is up to seven years, with a grace period of up to 12 months, and repayment may be monthly, quarterly or semi-annual, leaving room to align debt servicing with the rhythm of production and the seasonality of income. Loans are approved without a processing fee.

// The programme requires a clear level of financial discipline from applicants. The applicant must provide at least 20% own participation in the value of the land being purchased, must have no outstanding overdue obligations towards the Fund, AP Vojvodina or in respect of taxes and other public revenues, and the land being purchased must be within a 50-kilometre radius of the registered holding’s seat. In addition, the purchase must be completed within 12 months of signing the loan agreement. This is the clearest signal that the programme is intended for applicants with a defined investment intention, a sufficiently prepared transaction and a vision for future development. The loan collateral framework is relatively flexible, through two personal promissory notes and a commercial bank guarantee, or a first-ranking mortgage on agricultural land with an appropriate ratio of assessed value to loan amount.

// For holdings seeking to reduce fragmentation, rationalise cultivation and increase control over their own productive base, this credit line is a concrete development instrument. Land purchase in that sense is not merely an expansion of acreage, but an investment that can affect the organisation of work, operating costs and the long-term stability of production. This call therefore deserves the attention of producers thinking several seasons ahead and who see the strengthening of their holding through gradual but lasting consolidation of resources. More broadly, this credit line should also be viewed in the context of the incremental consolidation of agricultural land as an important precondition for more efficient and competitive production. The announced adoption of a dedicated land consolidation law is a further indicator that the state has recognised land consolidation and more rational land use as an important development direction. In that wider context, this credit line of the Development Fund of Vojvodina, while not formally part of the same initiative, moves in the same direction, supporting the gradual consolidation of holdings at the level of the farm itself through the financing of land purchases.For an assessment of the viability of your investment in additional parcels and projections of the effects on business performance, Glenfield has substantial experience and a well-developed methodology. Get in touch for an initial consultation and support.

Disclaimer: this report was prepared and published under the authority of Glenfield Training and Consulting Ltd. and is used only for informational purposes. Information that is used, have been obtained from sources that Glenfield Training and Consulting Ltd. believes to be reliable, but no guarantees their accuracy and completeness. None of the information or the proposal cannot be construed as an offer or solicitation to buy or sell. No part of this publication may be reproduced without written permission Glenfield Training and Consulting Ltd.